News

News

2020-10-12

A comprehensive guide for foreigners doing business in India

By Arpita Dutta, Legal Consultant, Louis International Patent Office

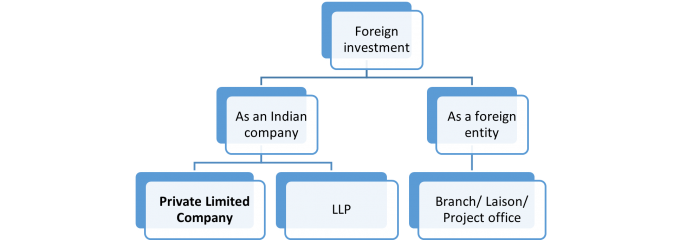

A foreign company needs local legal person and he/she need not be a shareholder. Indian Laws allow foreigner to keep 100% ownership by subscribing shares of Indian company. A foreign Company can become a Parent company of the Indian Subsidiary holding 100% shares.

A company must incorporate under the Companies Act 2013 of India in the following ways:

A foreign company needs local legal person and he/she need not be a shareholder. Indian Laws allow foreigner to keep 100% ownership by subscribing shares of Indian company. A foreign Company can become a Parent company of the Indian Subsidiary holding 100% shares.

A company must incorporate under the Companies Act 2013 of India in the following ways:

| As an Indian company |

Private Limited Company |

100% FDI, under the automatic route in many industries |

| Incorporate as owned subsidiary or joint venture | ||

| Minimum 2 Directors and 2-200 shareholders | ||

| One of Director must be both an Indian Citizen and Indian Resident. But he/she might not be a shareholder of the Company. | ||

| Approval from appropriate individual Govt Authorities | ||

| Limited Liability Partnership (LLP) | Partnership based on an agreement | |

| Minimum two partners required, who shall be individuals and one of them must be a person resident in India | ||

| Partner’s liability up to agreed contribution | ||

| Required approval by RBI | ||

| As a Foreign entity |

Branch Office |

Limited to the activity as parent company is engaged |

| Required approval by RBI | ||

| Liaison Office | cannot undertake any commercial activity | |

| Required approval by RBI | ||

| Project Office | Can execute only specific projects as approved | |

| Required approval by RBI |